The U.S. government is currently sitting on billions of dollars that belong back in your company's accounts. Since the Supreme Court terminated IEEPA tariffs on February 24, 2026, importers have already filed claims for $90 billion in overpaid duties. You've worked too hard on your margins to let List 3 and List 4a tariffs drain your liquidity. It's time to stop viewing these costs as a permanent loss and start reclaiming what's rightfully yours.

This guide explains exactly how to secure a tariff refund for the apparel and textile industry by leveraging the recent legal shift to recover Section 301 duties with zero upfront risk. We'll clarify which specific textile HTS codes are eligible for recovery and why this process is far more powerful and direct than a standard duty drawback. You'll discover a streamlined, hands-off filing process that restores your capital just in time to reinvest in the 2026-2027 season.

Key Takeaways

- Analyze the massive financial impact of List 3 and List 4a tariffs and why the apparel sector is the primary candidate for large-scale recovery.

- Learn how the landmark 2026 IEEPA ruling invalidated specific Section 301 duties, creating a fleeting opportunity to reclaim overpaid capital.

- Identify the specific HTS codes and documentation required to successfully secure a tariff refund for apparel and textile industry participants.

- Discover why specialized litigation-based recovery differs from standard customs brokerage and why it's necessary for navigating complex federal filings.

- Understand the benefits of a contingency-based partnership that eliminates upfront financial risk while prioritizing your brand's successful recovery.

The Financial Toll of Section 301 Tariffs on Apparel and Textiles

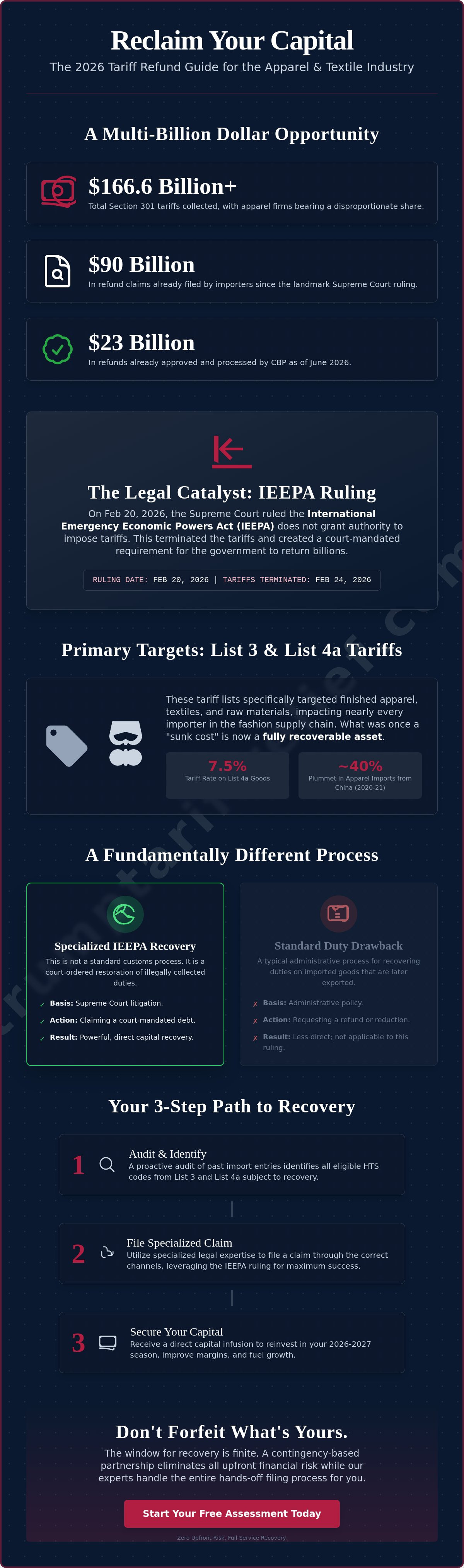

For nearly a decade, the fashion industry has functioned as an involuntary financier for federal trade policy. Since the initial implementation of duties under Section 301 of the Trade Act of 1974, over $166.6 billion has been collected from U.S. importers as of mid-2019. Apparel and textile firms bore a disproportionate share of this weight, often paying higher effective rates than other manufacturing sectors. By 2024 and 2025, these costs weren't just line items; they were the primary reason for shrinking retail margins and stalled seasonal growth.

The current legal landscape has shifted the narrative from compliance to recovery. The recent ruling regarding the International Emergency Economic Powers Act (IEEPA) suggests that the federal government exceeded its statutory authority when it expanded these tariffs. This creates a critical window for any firm seeking a tariff refund for apparel and textile industry imports. What was once considered a "cost of doing business" is now a reclaimable asset waiting to be audited and recovered.

List 3 and List 4a: The Textile Industry Targets

List 3 and List 4a specifically targeted the finished goods and raw materials that form the backbone of the fashion supply chain. List 4a goods, which include a vast array of consumer apparel, faced a 7.5% tariff rate that fundamentally altered sourcing strategies between 2019 and 2022. Because these categories covered such a broad spectrum of HTS codes, almost no textile importer escaped the financial drain. One study estimated that apparel imports from China plummeted by nearly 40% in 2020 and 2021 as a direct result of these specific duties. These lists are now the focal point of the refund portal because they represent the most egregious examples of executive overreach.

The Shift from Sunk Cost to Recoverable Asset

Most brands spent years trying to "manage" these tariffs by diversifying supply chains away from China, yet the historical debt remains on the books. A proactive audit of past import entries is no longer optional; it's a financial necessity for 2026 operations. Successfully securing a tariff refund for apparel and textile industry payments can provide a massive capital infusion. This liquidity allows brands to reinvest in the 2026-2027 season without taking on additional high-interest debt. It's about righting a financial wrong that should never have occurred.

Understanding the IEEPA Ruling and the 2026 Refund Portal

The path to a tariff refund for apparel and textile industry imports was paved by a landmark legal challenge against executive overreach. On February 20, 2026, the U.S. Supreme Court delivered a definitive ruling: the International Emergency Economic Powers Act (IEEPA) does not grant the President the authority to impose tariffs. This decision effectively dismantled the legal foundation used to expand Section 301 duties. As a direct result, all tariffs imposed under the IEEPA were terminated on February 24, 2026, creating a court-mandated requirement for the federal government to return billions in overpaid duties.

This isn't a typical administrative change; it's a judicial correction of a financial wrong. While the government has collected approximately $166 billion in Section 301 tariffs, the IEEPA ruling specifically targets the portions that exceeded statutory limits. The 2026 timeline is tight. U.S. Customs and Border Protection (CBP) has already begun processing claims, with roughly $23 billion in refunds approved as of June 2026. The opening of the dedicated refund portal in April 2026 marked the start of a finite window. If your firm hasn't yet cross-referenced its import data against the Harmonized Tariff Schedule of the United States, you're risking a permanent loss of capital.

How the IEEPA Ruling Differs from Section 301

It's vital to distinguish between the original intent of Section 301 and the mechanism of the current recovery. Section 301 was designed to address unfair trade practices, but the government used the IEEPA as a "workaround" to escalate tariff rates without following standard procedural requirements. Because the Supreme Court found this expansion illegal, the resulting IEEPA Explained framework focuses on court-ordered restoration rather than a standard policy shift. You aren't asking for a favor; you're claiming a court-mandated debt. If you're unsure if your past entries qualify, you can start a preliminary assessment here to identify your recoverable assets.

The Role of the Court of International Trade (CIT)

The Court of International Trade acts as the enforcement arm for this refund process. For apparel importers who were previously denied exclusions or found themselves trapped in the "List 3" and "List 4a" categories, the CIT's involvement is a game-changer. The judiciary has stripped away the government's ability to arbitrarily deny these claims based on trade politics. The CIT’s ongoing oversight ensures that the federal government maintains a transparent and fair filing process throughout the 2026 recovery cycle. This judicial pressure is why CBP is moving quickly to approve the $90 billion in claims already filed by proactive importers.

Specialized Recovery vs. Standard Customs Brokerage

Most apparel brands rely on their customs broker for every facet of international trade. It's a logical partnership for daily operations, but the 2026 IEEPA ruling has created a situation that falls far outside the scope of standard brokerage. While your broker is an expert in compliance and entry filing, they aren't built for high-stakes litigation recovery. Relying on a generalist to secure a tariff refund for apparel and textile industry duties often leads to missed deadlines and incomplete filings. This is a court-ordered reclamation, not a routine administrative task.

The distinction lies in the objective. A broker's primary goal is to keep your goods moving and ensure you're in compliance with current regulations. They look forward. Recovery specialists, however, look backward. We perform deep-dive audits into years of historical data to identify every cent of overpaid duty. The 2026 portal requires a level of technical precision and legal advocacy that standard brokerage firms simply aren't staffed to provide. If you wait for your broker to "get around" to these complex filings, you risk missing a finite window of opportunity.

The Limitations of Routine Compliance

Customs brokers often avoid the liability associated with filing complex refund protests. Because these claims are based on litigation rather than standard policy, they carry a different level of legal scrutiny. There's also a significant technical gap between a standard duty drawback and IEEPA recovery. A duty drawback is a common administrative process for exported goods; IEEPA recovery is a specialized legal action designed to right a specific regulatory wrong. You can see the breakdown of these differences in our guide on How it Works. Most brokers simply don't have the incentive to take on the heavy lifting required for these one-time recovery events.

Advantages of a Dedicated Recovery Partner

High-volume apparel importers often deal with thousands of entries across various HTS codes. Manually auditing these records requires sophisticated data-mining capabilities that go beyond a broker's standard software. A dedicated partner identifies eligible goods within HTS Chapters 61 and 62 with surgical precision, ensuring no recoverable asset is left behind. We also handle the significant "burden of proof" required by the 2026 portal, managing the complex documentation and federal filings on your behalf. By choosing a specialist, you ensure that your claim for a tariff refund for apparel and textile industry payments is maximized and filed with the professional confidence required to win.

Identifying Eligible Goods: HTS Codes and Textile Documentation

Securing a tariff refund for apparel and textile industry duties requires more than just a general desire for recovery. It demands granular precision at the HTS level. Because the IEEPA ruling specifically targets the expansion of Section 301 duties, your claim's success hinges on your ability to isolate eligible entries from thousands of historical records. This isn't a task for a manual audit; it's a data-intensive process that requires deep familiarity with the Harmonized Tariff Schedule and the specific tranches of the trade war.

Most eligible goods for fashion importers are concentrated within HTS Chapters 61 and 62. These chapters cover the vast majority of knitted and woven apparel that faced the 7.5% to 25% duty rates imposed during the 2018-2022 period. If your company imported finished garments or specific textile components from China during this window, you likely have significant capital tied up in federal accounts. Identifying these "recoverable assets" is the first step toward restoring your brand's liquidity.

The HTS Code Audit: What Apparel Brands Need

The audit process focuses heavily on Chapter 61 (knitted or crocheted apparel) and Chapter 62 (articles of apparel that are not knitted). Within these chapters, we look for items specifically swept into List 3 and List 4a. List 4a was particularly aggressive, targeting consumer-ready apparel that had previously been shielded from the trade war. The CBP Form 7501 is the indispensable legal document that validates the exact date, value, and tariff rate paid for every individual shipment entering the country. Without a verified Entry Summary, your claim lacks the foundational evidence required by the Court of International Trade.

Documentation Management for High-Volume SKUs

High-volume apparel brands often manage thousands of SKUs across multiple seasons. Organizing this volume of data for a single 2026 filing is a massive undertaking. Digital record-keeping is the backbone of a successful claim, as the 2026 portal requires entry-by-entry verification rather than bulk estimates. We manage this data-heavy task by cross-referencing your commercial invoices with CBP records to ensure every line item meets the specific "burden of proof" required for recovery. This meticulous approach eliminates common pitfalls, such as HTS misclassification or missing documentation, which frequently lead to claim rejections.

If you're ready to see which of your entries qualify for recovery, you can request a specialized Tariff Eligibility Assessment today. Our team handles the heavy lifting of data-mining and documentation verification, allowing your staff to focus on the upcoming season while we secure your refund.

Secure Your Refund with a Contingency-Based Partnership

The window to secure a tariff refund for apparel and textile industry imports is closing as the 2026 statute of limitations approaches. Most firms hesitate to pursue recovery because they fear the administrative burden or the high cost of specialized legal counsel. We've eliminated these barriers by operating on a "No Win, No Fee" contingency model. This structure ensures our interests are perfectly aligned with yours; we only succeed when we successfully restore your capital. You aren't just hiring a service provider; you're engaging a high-performing partner that takes on the risk while you reap the rewards.

This is about righting a financial wrong without adding to your overhead. Since the federal government was found to have exceeded its authority, the burden of restoration shouldn't fall on your shoulders. By choosing a partnership based on results, you ensure that your recovery efforts are handled by experts who are motivated to maximize every claim. We do the work, we manage the bureaucracy, and we only get paid when the check is in your hands.

Eliminating Upfront Costs and Risks

Traditional trade law firms often charge high hourly fees that drain your liquidity before a single dollar is recovered. This model is often a non-starter for firms with tight 2026 budgets. Our contingency structure removes this obstacle entirely. There are no upfront costs, no hidden consulting packages, and no financial risk to your balance sheet. Our transparency is our strength; the success-fee structure is clearly defined from day one, allowing you to categorize this recovery as a pure gain for your 2026-2027 operations.

Your Recovery Roadmap: From Assessment to Refund

Navigating the 2026 refund portal requires a steady, experienced hand. We follow a methodical 4-step process to ensure no recoverable asset is left behind:

- Assessment: We perform a preliminary audit of your HTS Chapters 61 and 62 entries to identify recoverable duties.

- Documentation: Our team gathers and verifies your CBP Form 7501 records and commercial invoices to meet the federal "burden of proof."

- Filing: We manage the complex litigation-based submission through the specialized 2026 portal.

- Recovery: We track the claim through the Court of International Trade oversight until the refund is issued to your accounts.

If you have specific questions about the filing window or how we handle high-volume data, visit our FAQ page for detailed answers. The time to act is now. Every day you wait is a day that your capital remains in federal accounts rather than fueling your next seasonal launch. Start your free eligibility assessment with Trump Tariff Relief today and reclaim your share of the billions in overpaid duties.

Reclaim Your Capital and Reinvest in Your Brand’s Future

The 2026 IEEPA ruling has transformed billions in overpaid duties from a sunk cost into a recoverable asset. For apparel and textile importers, this is a rare opportunity to right a financial wrong and restore liquidity for the upcoming seasons. Success requires moving beyond standard compliance to a specialized, litigation-based approach that focuses on the precise HTS codes within Chapters 61 and 62. Securing a tariff refund for apparel and textile industry payments is now a court-ordered reality, but the window to file is finite.

Trump Tariff Relief provides the specialized expertise in Section 301 litigation and comprehensive documentation management required to win. Our contingency-based model means you only pay if we recover your money, removing all financial barriers to entry. We take on the heavy lifting of data-mining your historical entries so your team can focus on growth. Don't let your hard-earned margins sit in federal accounts any longer. Get Your Free Apparel Tariff Refund Assessment today and start the process of reclaiming what’s yours. Your capital belongs in your business, and we're here to help you bring it home.

Frequently Asked Questions

Is the apparel and textile industry specifically included in the IEEPA refund ruling?

Yes, the apparel sector is one of the primary beneficiaries of this landmark ruling. Because List 3 and List 4a were created through an expansion of executive authority that the Supreme Court found illegal, the textile goods within those lists now qualify for recovery. This includes a massive range of finished garments and raw materials found in HTS Chapters 61 and 62. If you paid duties on these specific lists, your firm is eligible to file for a refund.

How far back can I go to claim refunds on textile imports?

You can generally target entries dating back to the initial implementation of List 3 and List 4a in 2018 and 2019. The ruling covers the entire duration these illegal tariffs were in place until their termination on February 24, 2026. This multi-year window allows for a significant tariff refund for apparel and textile industry participants who maintained high import volumes throughout the peak of the trade war.

What is the deadline for filing an IEEPA tariff refund claim in 2026?

The federal refund portal opened in April 2026, and the window for filing is legally finite. While the specific deadline for each entry is tied to its liquidation date and the statute of limitations, most experts urge filing before the end of the 2026 calendar year. Waiting too long risks your entries falling outside the recoverable period, making immediate action a financial necessity for your brand's liquidity.

Can I still claim a refund if my company already used duty drawback?

Yes, you can still pursue a refund, but the process requires careful auditing to avoid "double dipping." Standard duty drawback is an administrative process for exported goods, whereas this is a court-ordered recovery of illegally collected funds. We specialize in isolating the specific Section 301 duties that haven't been recovered through other mechanisms, ensuring your claim remains compliant while maximizing your total return.

How long does the federal government take to process apparel industry refunds?

Processing speeds vary, but U.S. Customs and Border Protection has already demonstrated a commitment to moving quickly. As of early June 2026, CBP has approved approximately $23 billion in refunds. For a tariff refund for apparel and textile industry claim, the speed of your payout often depends on the accuracy of your HTS data and the completeness of your documentation at the time of filing.

What happens if I don’t have all my original import documentation from 2019?

Don't let missing paperwork stop your recovery efforts. While original invoices are helpful, our team can often reconstruct your import history using federal entry summaries (CBP Form 7501) and other digital records. We provide comprehensive customs documentation management to bridge these gaps. We work directly with the necessary data sources to ensure your 2019 entries are verified and included in your 2026 filing.

Are there specific HTS codes in the textile sector that are excluded from this refund?

Eligibility is determined by the legal authority used to impose the tariff rather than the HTS code alone. While most apparel in Chapters 61 and 62 is eligible if it was part of List 3 or List 4a, goods imported under List 1 or List 2 may fall under different legal parameters. A detailed Tariff Eligibility Assessment is required to confirm which specific codes in your portfolio qualify for the IEEPA-based recovery.

Do I need to pay any upfront fees to start the recovery process with Trump Tariff Relief?

No, you don't pay anything out of pocket to begin the process. We operate on a strictly contingency-based model, which means our fee is a percentage of the money we actually recover for your business. This removes the financial barrier to entry and ensures we're fully motivated to win your case. You get the benefit of our specialized litigation expertise without any upfront risk to your 2026 budget.

Ready to find out what your business may be owed?

Check My Eligibility