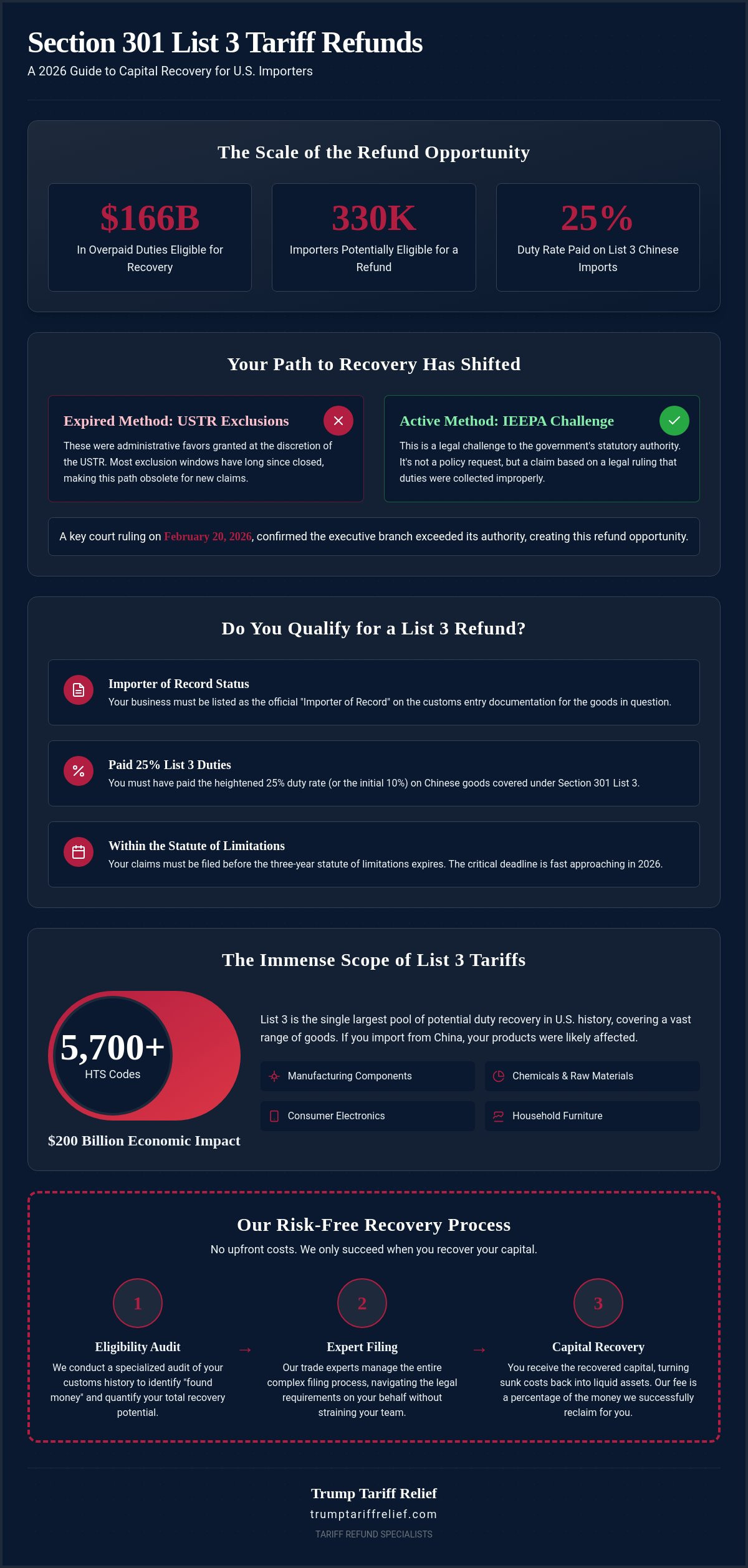

Approximately 330,000 importers are currently eligible to reclaim a share of $166 billion in duties overpaid under invalidated executive authorities. While many businesses have written off the 25% duties paid on Chinese imports as a permanent loss, the legal landscape shifted decisively on February 20, 2026. If you're seeking a Section 301 List 3 tariff refund, it's vital to recognize that the window for recovery is now driven by statutory authority challenges rather than the policy exclusions of the past.

We know the constant pressure of 25% duties has eroded your margins, and the lack of internal resources to audit thousands of entries makes recovery feel out of reach. This article outlines exactly how your business can navigate the complex IEEPA developments to recover millions in overpaid capital with zero upfront risk. We'll preview the specific 'yes or no' eligibility criteria and show you how to beat the 2026 statute of limitations, allowing you to turn those sunk costs back into liquid capital without straining your team.

Key Takeaways

- Differentiate between the concluded Section 301 litigation and the active IEEPA authority challenge that remains a viable path for capital recovery.

- Determine your eligibility by confirming your status as the Importer of Record and assessing whether your duty spend meets high-priority thresholds.

- Act before the 2026 deadline to ensure the three-year statute of limitations doesn't permanently bar your company's right to a refund.

- Uncover the "found money" opportunity within your customs history to file for a Section 301 List 3 tariff refund through our specialized documentation audit.

- Leverage a contingency-fee model that removes financial risk while our trade experts handle the complex management of your customs filings.

The State of Section 301 List 3 Tariff Refunds in 2026

List 3 wasn't just another trade policy. It was a $200 billion economic earthquake that fundamentally restructured how US businesses source from China. Leveraged under Section 301 of the Trade Act of 1974, this action initially imposed a 10% duty in September 2018. However, the burden intensified when the rate spiked to 25% in May 2019. This 15% increase turned manageable costs into massive liabilities for thousands of importers, effectively siphoning billions of dollars away from American innovation and payrolls into government accounts.

2026 has emerged as the "Year of Recovery" for impacted importers who refuse to accept these costs as permanent. While the Supreme Court declined to review the broad Section 301 case on June 15, 2026, a separate and successful legal battle regarding the International Emergency Economic Powers Act (IEEPA) has provided a lifeline. The February 20, 2026, ruling confirmed that the executive branch exceeded its statutory authority in specific instances. This development means a Section 301 List 3 tariff refund is a tangible financial recovery path for companies that acted as the Importer of Record during the peak of these trade actions; for businesses in the transport sector aiming to reinvest these recovered funds into enhanced fleet safety, visit ProPride, Inc..

What Goods Fall Under List 3?

The scope of List 3 is staggering, covering more than 5,700 unique HTS codes. This list includes everything from essential manufacturing components and chemicals to consumer electronics and household furniture. Because of this massive breadth, List 3 represents the largest single pool of potential duty recovery in US history. If your business imports finished goods or raw materials from China—including chemical and process equipment inputs where TEG Reclamation Services provides specialized support—there's a high probability your products are still carrying that 25% duty today. Verifying your specific HTS codes is the first step in identifying "found money" that can be reclaimed through a Section 301 List 3 tariff refund. Many CFOs are surprised to find that entries they liquidated years ago are now eligible for a full audit and recovery.

The Difference Between Exclusions and Legal Refunds

Many businesses mistakenly believe their refund opportunities died when the USTR's exclusion windows closed. Exclusions were administrative favors granted at the discretion of the USTR, and most have long since expired. The current recovery effort is different. It's based on a legal challenge to the government's authority under IEEPA. You aren't asking for a policy exception; you're participating in a process to recover capital that was collected without proper legal standing. This legal mechanism circumvents the restrictive exclusion process, offering a broader and more robust way to restore your margins. To see the specifics of how this authority challenge works, you can explore our guide on how IEEPA explained functions for importers. This shift from administrative requests to statutory claims is why recovery is finally possible in 2026.

Understanding the IEEPA Challenge: The Key to Your Refund

The International Emergency Economic Powers Act (IEEPA) serves as the primary statutory vehicle for these claims, acting as the legal lever to overturn tariffs that were implemented without explicit Congressional authorization. While the Official Section 301 Tariff Actions were initially framed as a standard enforcement of trade policy, the subsequent expansion into List 3 bypassed critical procedural safeguards. This overreach created the foundation for the current recovery efforts. For business owners, the "IEEPA challenge" isn't just a legal technicality; it's the specific mechanism that allows us to bypass the now-closed door of USTR exclusions and target the illegal collection of duties at the source.

The core of the argument rests on whether the executive branch possessed the authority to modify existing trade actions to such an extreme degree without fresh investigations. When the government moved from a 10% duty to a 25% duty on $200 billion worth of goods, it relied on emergency powers that the courts have now scrutinized. This shift in the legal landscape has effectively moved the burden of proof from the importer to the government, opening a window for a Section 301 List 3 tariff refund that many had previously assumed was impossible. If you're unsure if your specific entries fall under these authority challenges, you can request an eligibility assessment to identify your total recovery potential.

The Landmark Rulings Impacting 2026 Claims

The momentum for recovery reached a fever pitch following the February 20, 2026, Supreme Court decision. This ruling invalidated specific tariffs imposed under IEEPA, confirming that the executive branch had indeed exceeded its statutory bounds. This wasn't a minor administrative correction; it was a fundamental rebuke of how trade taxes were being levied. For importers, this created a binding precedent for retroactive capital recovery. You can learn more about the IEEPA explanation and how these specific court victories translate into credits or cash for your business. These rulings have turned what was once a speculative legal theory into a structured, government-mandated refund process.

Why This Isn't a Standard 'Duty Drawback'

It's vital to distinguish this process from standard customs procedures like duty drawback. Traditional drawback is a compliance-based refund for goods that are re-exported. In contrast, the Section 301 List 3 tariff refund is a litigation-driven recovery of capital that was collected unlawfully. Most customs brokers are focused on day-to-day compliance and entries; they don't have the legal infrastructure to file the necessary "Protests" and "Summons" required to secure your spot in the refund queue. Securing your capital requires a specialized legal strategy that goes beyond simple documentation. It involves positioning your firm within the ongoing litigation to ensure that when the final disbursements are made, your claims are already verified and protected against the statute of limitations.

While specialized legal teams work on recovering your capital, maintaining an efficient supply chain is equally vital; ICAT Detroit provides the global freight expertise required for the time-critical and high-value cargo typically impacted by these tariffs.

Eligibility Audit: Does Your Business Qualify for List 3 Recovery?

To secure a Section 301 List 3 tariff refund, the first and most critical hurdle is establishing legal standing. You must be the Importer of Record (IOR). This means your company's name and tax identification number are the ones registered on the CBP entry forms. Even if your supplier paid the duties on your behalf as part of a "DDP" (Delivered Duty Paid) agreement, the supplier, not your firm, likely holds the legal right to the refund. It's a common point of confusion that can derail a recovery effort before it starts.

Scale is the second major factor in the audit process. While any overpayment is a wrong that deserves correction, the complexity of the legal challenges to IEEPA tariffs means that businesses with over $1 million in total duty spend are the highest priority for recovery. These larger claims justify the extensive forensic audit work required to identify and verify every eligible entry. Manufacturing, retail, and technology sectors are particularly well-positioned because their supply chains were the primary targets of the original List 3 action. If your margins have been squeezed by the 25% duties on components or finished goods, you're exactly who the court's decision was intended to help.

Finally, your business must meet the "clean hands" requirement. This means your customs documentation must be audit-ready and compliant. If your HTS classifications are inconsistent or your valuation methods are questionable, it can complicate the recovery process. Our Customs Documentation Management ensures your filings are precise, protecting your claim from government scrutiny while maximizing the total capital we can identify for recovery.

High-Priority HTS Codes for List 3

List 3 was designed to be broad, but certain categories bore the brunt of the 25% duties. High-priority goods include consumer durables, automotive parts, and a vast array of electronics components. You should cross-reference your internal import logs against the master List 3 HTS schedule to identify every dollar paid since May 2019. If you aren't sure how to read your ACE reports or identify these specific codes, check our FAQ for eligibility questions to see how we simplify this search. Identifying the right codes is the difference between a successful Section 301 List 3 tariff refund and a missed opportunity.

The 'Importer of Record' Trap

The check always goes to the entity that filed the paperwork. If your corporate structure has changed through a merger or acquisition since 2018, the right to the refund must be clearly traced through the transaction documents. We've seen many businesses lose out because they didn't account for these successor-in-interest rights during a buyout. Our specialized Tariff Eligibility Assessment process clarifies these legal webs, ensuring the recovery ends up in your bank account rather than a former supplier's or a defunct entity's. You can see how this works by reviewing our Tariff Eligibility Assessment workflow to ensure your claim is filed correctly the first time.

The 2026 Deadline: Navigating the Statute of Limitations

Time is the most ruthless adversary in trade litigation. For importers seeking a Section 301 List 3 tariff refund, the 2026 calendar represents a critical "cliff edge" due to the three-year statute of limitations from the date of entry liquidation. For many entries liquidated in 2023, the final opportunity to file a claim is expiring this year. The deadline for 2026 filings is non-negotiable. If you miss this window, the government's right to keep your capital becomes absolute, regardless of how favorable future court rulings might be.

Waiting for the perfect moment is a high-stakes gamble that often leads to the legal defense of "laches," where the government argues that your delay has prejudiced their ability to process the claim. To prevent this, sophisticated importers are "tolling" the statute of limitations by filing protective claims now. This action effectively freezes the clock and preserves your right to recover capital from entries that would otherwise age out of the system. Your ability to secure a Section 301 List 3 tariff refund depends entirely on your speed in identifying these expiring entries and submitting the necessary summons to the court.

Why You Can't Wait for the 'Final Verdict'

Many CFOs operate under the dangerous misconception that once a final court victory is announced, refunds will automatically flow back to every impacted business. This isn't how the system works. U.S. Customs and Border Protection (CBP) processes refunds on a "First-in, First-out" basis, and they only pay those who have active, legally preserved claims. You can read about the Statute of Limitations in detail to understand why being at the back of the line is a recipe for failure. If you don't have a claim on file when the final disbursements are ordered, you'll likely be barred from recovery.

The Countdown: Critical Dates for List 3 and 4a

The remaining window for 2026 recovery is shrinking daily. We're already seeing CBP issue documentation requests to early filers who moved quickly after the February 2026 Supreme Court ruling. This increased activity suggests that the government is preparing for a surge of filings, and those who wait until the final quarter of the year will face significant processing bottlenecks. The urgency of a Tariff Eligibility Assessment cannot be overstated; it's the only way to beat the rush and ensure your documentation is verified before the statutory clock runs out. Don't let your company's capital stay in the government's coffers because of a missed deadline.

Secure your spot in the recovery queue today by requesting a preliminary audit of your 2023 and 2024 entries.

Risk-Free Recovery: The Trump Tariff Relief Process

Most businesses hesitate to pursue overpaid duties because they fear the high cost of specialized legal counsel. Traditional trade law firms often charge significant hourly rates, creating a financial barrier that prevents mid-sized companies from claiming what's rightfully theirs. We've eliminated that barrier. Our process is built entirely on a contingency-fee model, meaning we only get paid if we successfully secure your capital. This turns the pursuit of a Section 301 List 3 tariff refund from a legal gamble into a high-reward financial audit with zero upfront risk to your bottom line.

Our team provides end-to-end management, covering every technical detail from the initial HTS audit to the final court filing. We understand that your internal finance team is already stretched thin. By serving as your active engine for recovery, we remove the administrative burden and the need for internal forensic accounting. We handle the complex Customs Documentation Management requirements to ensure your claims are not only filed quickly but are also fully compliant with current CBP standards. This comprehensive approach ensures that the path to recovery is seamless and professional; if you are also looking for specialized freight support to strengthen your supply chain, visit Tranzit Express Inc..

Step 1: The Preliminary Recovery Audit

The journey begins with a forensic look at your import history. We identify missed opportunities within your past five years of entries, searching for specific HTS codes that were caught in the crossfire of statutory overreach. The best part? This initial assessment is completely no-cost. We do the heavy lifting to determine exactly how much capital your firm is eligible to reclaim before you ever commit to the process. You can see how it works in more detail to understand our methodology for identifying "found money" in your customs logs. If there's no recovery potential, you've lost nothing but a few minutes of time.

Step 2: Filing and Advocacy

Once we've identified your eligible entries, our experts take the lead in interfacing with U.S. Customs and the Court of International Trade (CIT) on your behalf. We manage the entire lifecycle of the "Protests" and "Summons" required to toll the statute of limitations. Our contingency model ensures total transparency. There are no hidden fees, no hourly billing, and no surprise invoices. We're fully invested in your success because our compensation is directly tied to the results we deliver. Don't let the 2026 deadline pass while your capital remains in government hands. Secure your Section 301 List 3 Refund Assessment today and let our team start the work of restoring your margins.

Secure Your Capital Before the 2026 Statutory Window Closes

The opportunity to reclaim overpaid duties is no longer a matter of administrative favor; it's a legal right established by recent authority challenges. By identifying your status as the Importer of Record and auditing your high-priority HTS codes, you can transform years of sunk costs back into liquid capital. Reclaimed funds can be used to explore new financial horizons, such as the institutional funding opportunities available through TradeFundrr, but you must act before the 2026 statute of limitations permanently bars your recovery.

Securing a Section 301 List 3 tariff refund doesn't have to be a drain on your internal resources or your budget. Our expert-led team handles the comprehensive management of all customs and CIT documentation on a contingency basis. You pay nothing unless we recover your funds. We're ready to serve as your advocate and navigator through this complex bureaucracy, taking on 100% of the financial risk to ensure justice for your business.

Claim Your Risk-Free List 3 Refund Assessment Now

It's time to stop letting the government hold your capital; let's start the process of restoring your financial strength today.

Once you have restored your margins through these refunds, you can reinvest that capital into growth; for instance, you can explore Impact Post Card – 6 X 11 from We Mail America to launch a high-impact direct mail campaign.

Similarly, companies looking to scale their physical product lines can utilize Iris DTF for high-quality custom transfers and stickers that provide a professional finish to any merchandise.

Frequently Asked Questions

Is the Section 301 List 3 refund a real program or a scam?

This is a legitimate legal recovery process based on federal court rulings. The U.S. Court of International Trade and the Supreme Court have issued specific decisions regarding the executive branch's use of statutory authority. It isn't a government "grant" program but a litigation-driven reclamation of capital collected under invalidated authorities. Thousands of American importers are currently filing legal summons to protect their right to these court-mandated refunds.

How much money can my business expect to recover from List 3 tariffs?

Your recovery potential depends entirely on your total duty spend for goods imported under List 3 HTS codes since May 2019. For businesses with significant import volumes, the potential for a Section 301 List 3 tariff refund often reaches into the millions of dollars. We identify every eligible entry through a forensic audit of your ACE reports, ensuring that the 25% duties originally paid are fully accounted for.

What is the deadline to file for a Section 301 List 3 refund in 2026?

The deadline is dictated by a three-year statute of limitations from the date of liquidation for each individual import entry. For many entries liquidated in 2023, the window for recovery expires in 2026. Because liquidations happen on a rolling basis, there is no single final date. However, waiting risks losing the right to claim older, high-value entries that age out of the system every day.

Do I need to hire a lawyer to get my tariff money back?

While you don't need to hire an independent law firm on an hourly basis, you do need a partner capable of managing complex litigation and customs filings. Most standard customs brokers lack the legal infrastructure to file the required summons in the Court of International Trade. We provide a specialized team of trade and legal experts to handle the entire process on a contingency basis, removing the barrier of expensive legal fees.

What documents do I need to provide for a tariff recovery audit?

You typically need to provide access to your ACE (Automated Commercial Environment) data or detailed import logs. These records must include HTS codes, entry dates, liquidation dates, and the total duties paid. Our Customs Documentation Management team uses these files to cross-reference your imports against the master list of eligible goods. Having clean, audit-ready documentation ensures that CBP can verify your claim without unnecessary processing delays.

Can I still claim a refund if my product exclusion has already expired?

Yes, you can still claim a refund because the current recovery efforts are based on statutory authority challenges rather than administrative exclusions. Exclusions were temporary favors granted by the USTR, while the IEEPA challenge argues that the tariffs were levied illegally from the start. This means even if you were never granted an exclusion, or if yours expired years ago, you may still be eligible for a Section 301 List 3 tariff refund.

How long does the government take to process a tariff refund check?

Processing times vary based on the volume of claims and the status of final court mandates. Once the litigation reaches its final disbursement phase, CBP typically processes verified claims on a first-in, first-out basis. Filing your summons early positions your business at the front of the queue. While the government rarely moves with speed, having a legally preserved claim is the only way to ensure you eventually receive your check.

What is the difference between Section 301 and IEEPA refunds?

Section 301 refers to the trade law used to investigate foreign trade practices, while IEEPA is the emergency act used to implement the actual duty increases. The Supreme Court's February 20, 2026, ruling specifically targeted the misuse of IEEPA authority for these tariffs. While the initial Section 301 investigation was upheld, the specific mechanism used to raise the duties to 25% was found to be a statutory overreach, creating the refund opportunity.

Ready to find out what your business may be owed?

Check My Eligibility